Global chickpeas production continued to grow in the 2025/2026 season, marking the second consecutive season of supply expansion. Production is estimated to reach roughly 17.7 million metric tons in 2025/2026, representing an increase of about 1.4% compared to the 2024/2025 season. Australia remains the largest chickpeas exporter globally but supplying mainly Desi chickpeas to Asian markets. Canada, Russia, Turkey, Argentina and the United States remain the major exporters of Kabuli chickpeas worldwide.

In this article, we review the most important developments shaping the market in 2025/2026. We focus on production trends and market developments in the major exporting countries that are particularly important for the European market – Canada, Turkey and Russia. We will also briefly examine European chickpeas production, review the current situation in the organic chickpeas market, and conclude with a short market summary highlighting the key trends affecting buyers and suppliers.

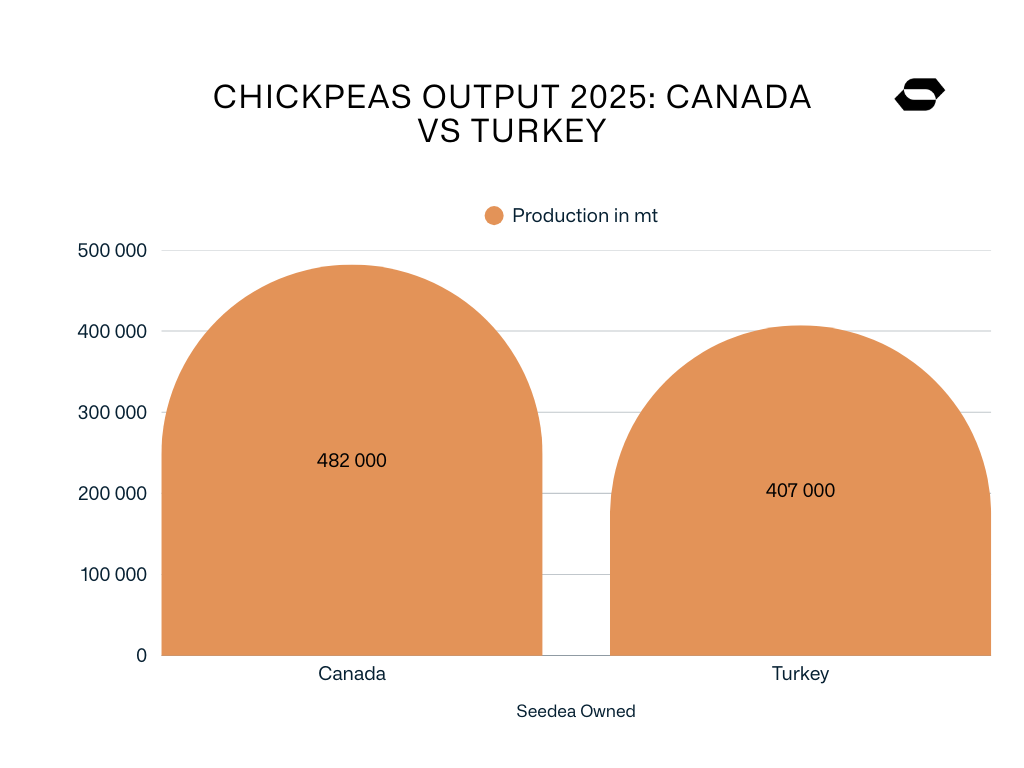

Canada Chickpeas Production

Canada remains one of the most important exporters globally. According to Agriculture and Agri-Food Canada, chickpea production increased significantly in the 2025/2026 season, reaching approximately 482 000 tons, compared with 287 000 tons in 2024/2025. The larger crop is mainly the result of increased planted area and good yields. Especially in Saskatchewan, which remains the main chickpea-producing province in Canada.

Despite the larger harvest, Canadian chickpea exports are expected to fall slightly, from 209 000 tons in 2024/2025 to around 200 000 tons in 2025/2026. Early trade data also shows that exports started the season at a slower pace than last year. Asia, European Union and Turkey continue to be the main destinations for Canadian chickpeas exporters.

With a larger crop and slower export pace, carry-out stocks are expected to increase, while the average price dropped from about 735 $ per ton in 2024/2025 to around 560 $ per ton in 2025/2026 due to higher global supply.

Turkey Chickpeas Production

Turkey remains one of the key producers of Kabuli chickpeas and very important supplier for European markets. According to the Turkish Statistical Institute (TÜİK), chickpeas production in 2025 reached around 407 000 tons, compared with about 580 000 tons in 2024.

Despite the smaller crop, Turkey continues to play an important role in international chickpeas trade. The country is not only an exporter of domestically produced Kabuli chickpeas but also an active trading hub, importing chickpeas from other origins – particularly Russia – and re-exporting them to nearby markets.

Looking ahead, market expectations for 2026 are more optimistic. Local industry sources report that farmers are increasing planted area after stronger pulse prices in previous seasons. If weather conditions remain favorable, Turkey could see a noticeable recovery in chickpeas production in the upcoming harvest.

Russia Chickpeas Production

Russia has become an increasingly important producer and exporter of chickpeas in recent years. According to industry reports, chickpeas harvest in 2025 exceeded 620 000 tons, marking the third consecutive year of record production in the country.

The increase is mainly driven by expanding planted area and strong yields in southern regions such as Volgograd, Saratov and the Stavropol region, where chickpeas have become an attractive crop for farmers due to stable export demand.

Russia exports chickpeas primarily to Turkey, Pakistan, India, Egypt and several Middle Eastern markets. Part of the crop exported to Turkey is further traded to other destinations, which makes Russia an important supplier for the wider chickpeas trade, including markets connected to Asian and Middle East.

Related article: Chickpeas Market Update – October 2024

European Chickpeas Production

Chickpeas production in Europe remains relatively limited compared with the major global exporters, but several countries continue to supply regional markets.

Spain Chickpeas Production

Spain, the largest producer within the European Union, recorded a significant decline in 2025, with production falling to around 56 100 tons, compared with 82 700 tons in 2024. The drop was mainly linked to reduced planting area and unfavorable weather conditions, including drought periods in some key producing regions such as Castilla y León, which affected yields during the growing season.

Italy Chickpeas Production

In Italy, chickpeas production in 2025 was estimated at around 48 000 – 50 000 tons, slightly lower than the approximately 52 000 tons harvested in 2024. Italian chickpeas production remains concentrated in southern regions, where the crop is well suited to dry conditions and continues to benefit from stable domestic demand.

France Chickpeas Production

France remains a smaller but stable producer within the EU pulse sector. Production in 2025 is estimated at around 20 000 tons, slightly below the about 21 000 tons recorded in 2024. French chickpeas production is mainly located in southern regions such as Occitanie and Provence, where the crop fits well into crop rotation systems focused on soil improvement and diversification.

Organic Chickpeas Market

The organic chickpeas market remains relatively small compared with conventional production but continues to attract growing interest from buyers in Europe. Turkey is currently largest supplier of organic chickpeas, benefiting from its exports. Turkish organic chickpeas are widely exported to European markets.

Within the European Union, organic chickpeas are produced mainly in Italy, which remains the largest producer in this segment. France is another important supplier, with organic chickpeas increasingly integrated into crop rotations as part of sustainable farming systems. Although production volumes remain limited, the organic chickpeas market continues to develop and is a segment worth monitoring in the coming years.

Chickpeas Summary

Europe’s chickpea picture into early 2026 starts with Spain: the 2025 advance points to a smaller crop than in 2024. At the same time, the 2025/2026 season has become challenging for exporters, as multiple origins are competing on the market. Many producing countries are competing on the market at the same time – including Canada, Turkey, Russia, as well as Argentina and Mexico.

This strong competition has been putting pressure on prices, which have been gradually decreasing almost every month during the season. As a result, larger stocks may remain available and could carry into the beginning of the 2026 harvest.

In the organic chickpeas segment, global production remains relatively low. At the same time, a large share of organic chickpeas is consumed within the European market, which creates opportunities for further development, especially for producers within the EU. The organic segment is still small, but it is definitely a market worth watching in the coming years.

Source:

- Agriculture and Agri-Food Canada – Outlook for Principal Field Crops 2026 https://publications.gc.ca/collections/collection_2026/aac-aafc/A77-1-2026-1-21-eng.pdf

- Manitoba Co-operator – Pulse Weekly Export Report https://www.manitobacooperator.ca/daily/pulse-weekly-canadian-pea-lentil-exports-slow-to-start-2025-26/

- Turkish Statistical Institute (TÜİK) https://veriportali.tuik.gov.tr/en/press/53938 https://veriportali.tuik.gov.tr/en/press/53939

- Gaziantep Sabah – agricultural outlook https://gaziantepsabah.com/guncel/hububatta-son-5-yilin-rekorunu-kirabiliriz/173378

- https://oleoscope.com/analytics/urozhaj-v-rossii-prevysit-proshlogodnij/

- https://riac34.ru/news/210009/

- https://agrotochka.org/post/urozhaj-nuta-v-rf-obnovil-rekord-tretij-god-podrjad-15369