The global lentil market continued to improve in the 2025 season, building on the recovery (already seen in 2024) after a weaker 2023. Canada harvested a much larger crop, supported by better yields, while Australia also returned with strong production after weather issues in the previous season. Turkey, on the other hand, recorded lower production, increasing its dependence on imports rather than influencing global supply.

At the same time, the season showed a clear shift in how lentils are traded. Canada and Australia remained the key global exporters, but regional flows became more important. Countries like Russia and Kazakhstan increased their presence in nearby markets such as Turkey, where logistics and shorter delivery times started to play a bigger role.

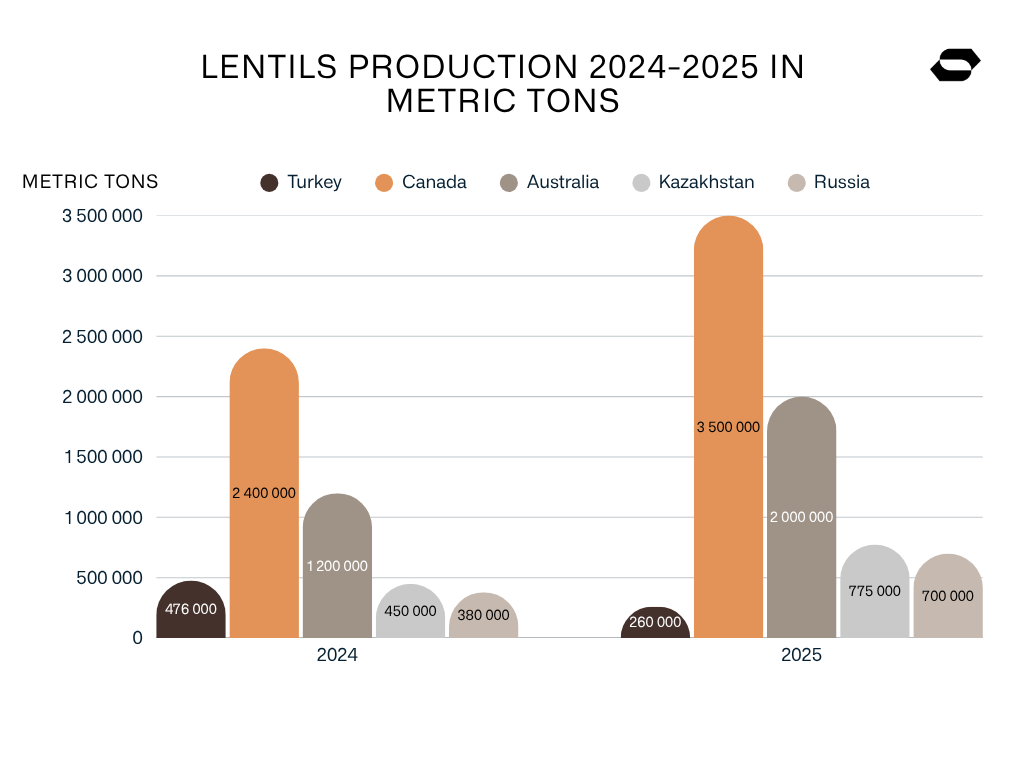

Global picture: clear growth from 2024 to 2025

The 2025 season confirmed a strong increase in global lentil production compared to 2024, continuing the recovery that already started after the weaker 2023 crop. Total output returned to a clearly comfortable level, driven mainly by higher production in export-oriented countries.

The growth was driven this season not only by Canada and Australia, which remain the key global exporters, but also by a strong increase in production in Kazakhstan and Russia. This added a new layer of supply, especially in regions closer to major import markets such as Turkey, Asia and Middle East countries.

Canada: strong crop, but rising stocks

Canada confirmed its position as the leading global lentil exporter in the 2025 season, with a significantly larger crop compared to 2024. The increase was mainly driven by higher yields, with Saskatchewan remaining the dominant production region.

- 2024: 2.43 million tonnes

- 2025: ~3.3–3.5 million tonnes (+35–40%)

Production structure:

- Red lentils: ~2.2–2.4 million tonnes

- Green lentils: ~0.6–0.7 million tonnes

- Other types: ~0.3 million tonnes

Canada continues to focus mainly on red lentils, which dominate global trade. With the larger crop, exports are expected to increase to around 2.0-2.1 million tonnes, with India and Turkey remaining the key markets, followed by the UAE, Bangladesh, and Egypt.

However, export growth is slower than the increase in production. As a result, ending stocks are projected to reach around 1.1-1.3 million tonnes, the highest level in recent years.

Related article: Lentils Market Update – March 2025

Australia: strong recovery in 2025/2026 and pressure on red lentils

Australia returned as a major supplier in the 2025 season, following a weaker previous year affected by weather issues.

- 2024: ~1.1–1.2 million tonnes

- 2025: ~1.8–2.0 million tonnes

The increase was driven by higher yields and improved growing conditions, with production returning closer to long-term levels. Australian production is strongly focused on red lentils, which play a key role in global trade, especially in price-sensitive markets.

With the larger crop, export availability increased significantly, strengthening Australia’s position in key destinations such as India and the Middle East. At the same time, Australia directly competes with Canada in these markets, particularly in the red lentil segment.

Geographical proximity gives Australia an advantage in freight to Asian markets, which improves its competitiveness during high supply periods. Strong crops in both Canada and Australia increased global availability and led to higher competition across export markets. As a result, lentil prices reached some of the lowest levels in recent years.

Turkey: key importer and regional trade hub

Turkey is not one of the largest global producers, but it remains one of the most important players in the lentil market due to its role as a major importer and re-exporter.

- 2024 production: ~476k tonnes

- 2025: 260k tonnes (huge decline)

Lower domestic production in 2025 increased Turkey’s dependence on imports and strengthened its position as a key buying market. In the 2025/2026 season, a clear shift in sourcing became visible. Alongside Canada, Turkey increased imports from regional suppliers, especially Kazakhstan and Russia.

Imports from both countries grew, supported by shorter transit times and more competitive logistics compared to overseas suppliers. This confirms a structural change, as Turkey is gradually shifting part of its sourcing from global (mainly Canada) suppliers toward regional origins.

Russia & Kazakhstan: rising regional supply power

The 2025 season brought a strong increase in lentil production in both Russia and Kazakhstan, making the region a much more relevant supply source.

- Russia: ~380k → ~700k tonnes (2025)

- Kazakhstan: ~450k → ~775k tonnes (record)

Kazakhstan recorded one of the fastest growth rates on the market, while Russia nearly doubled its production year-on-year. Together, both countries could reach a combined output of over 1.4 million tonnes.

At the same time, export activity increased. Kazakhstan exported around 425 thousand tonnes in 2025, with approximately 356 thousand tonnes going to Turkey, making it the key destination. Russia also strengthened its presence in Turkey but also in regional trade.

The result is a clear shift in the market structure. Russia and Kazakhstan are no longer secondary origins, but increasingly important suppliers, especially for nearby markets.

Organic lentils: tight supply despite higher global production

Organic lentils are still a smaller segment than conventional, but they remain structurally important in The organic lentil market in the 2025 season remains more complex than expected. While conventional production increased significantly, this did not translate into better availability or lower prices in the organic segment.

There is currently better availability of green organic lentils, but the situation for red lentils has been tight for several months. In recent weeks, demand has increased further, while raw material remains limited. Traditionally, Turkey was an important source, but availability there is also very restricted this season, leaving buyers mainly with European origins and limited stocks.

As a result, prices remain high. Organic red lentils (Crimson type) are reaching around 1,80-1,90 EUR/kg FCA (currently), reflecting the shortage of raw material. Despite higher global supply, the organic market remains constrained, and securing volume continues to be a challenge.

Lentils market summary

The 2025 lentil season confirmed a strong increase in global supply, driven by higher production in Canada and Australia, as well as rapid growth in Kazakhstan and Russia. At the same time, Turkey strengthened its role as a key importer, with sourcing increasingly shifting toward regional origins. Higher availability and strong competition between exporters pushed prices down, especially in red lentils, reaching some of the lowest levels in recent years.

Looking ahead, prices are likely to remain under pressure at least until the end of 2025, and possibly longer, as high stocks, particularly in Canada and Australia, still need to be absorbed. Demand from key markets such as India may remain limited due to strong domestic pulse production, especially chickpeas. This is no longer a shortage market, but a market of excess supply and competition.

At the same time, the organic segment continues to face supply challenges, with recurring shortages of raw material, particularly in the spring period, making sourcing consistently difficult.

Source:

- https://grainscanada.gc.ca/en/grain-research/grain-harvest-export-quality/lentils/2025/harvest-quality-report-lentils-2025.html

- https://www.agriculture.gov.au/abares/research-topics/agricultural-outlook/australian-crop-report/march-2026

- https://www.publicnow.com/view/9FC1D9B13DCE76971DE857316A8790AFB952015B?1766735257=&utm

- https://seedea.pl/lentils-market-update-march-2025/