China reduced acreage again in 2025, and the GWS segment remains structurally limited there. Austria delivered a stable crop on paper, but regional yield differences will ultimately determine how much The global pumpkin seeds market is changing. China remains the world leader in total pumpkin seed production, but the GWS segment continues to shrink. At the same time, Austria delivered solid 2025 harvest results, while Poland is strengthening its position as a strategic EU origin and a real alternative to China, offering shorter transit times, faster shipments and geographic proximity to European buyers.

Total volume may appear sufficient on paper. However, workable premium-grade GWS supply is tighter than many assume. Demand for EU-grown material is rising, and price pressure in recent weeks confirms that the market is heating up. In this update, we analyze the real situation in China, Austria and Poland, followed by a focused view on the organic pumpkin seeds segment.

China: Farmers Shift Away from GWS

China remains the largest pumpkin seed producer globally. However, reliable statistical transparency for 2025 is limited. Official data is either delayed or does not fully reflect the real production structure. In practice, market participants rely on direct supplier communication and field-level estimates.

What we know is clear: total pumpkin seed acreage in China declined significantly in 2025. Industry sources indicate a sharp reduction in cultivated area compared to 2024. The scale varies depending on the source, but all signals point in one direction – production was lower.

Several factors explain this contraction. Climate volatility, adjustments in agricultural policy and changing profitability all influenced planting decisions. Farmers continue to prioritize Shine Skin varieties and sunflower over GWS, as these crops offer stronger and more stable returns.

In the case of GWS, the decline appears structural rather than seasonal. The segment brings lower margins, higher cleaning costs and greater exposure to export-related claims. At the same time, compliance requirements from importing markets, especially the EU, are becoming stricter. As a result, GWS is gradually losing strategic importance within China’s pumpkin seed industry.

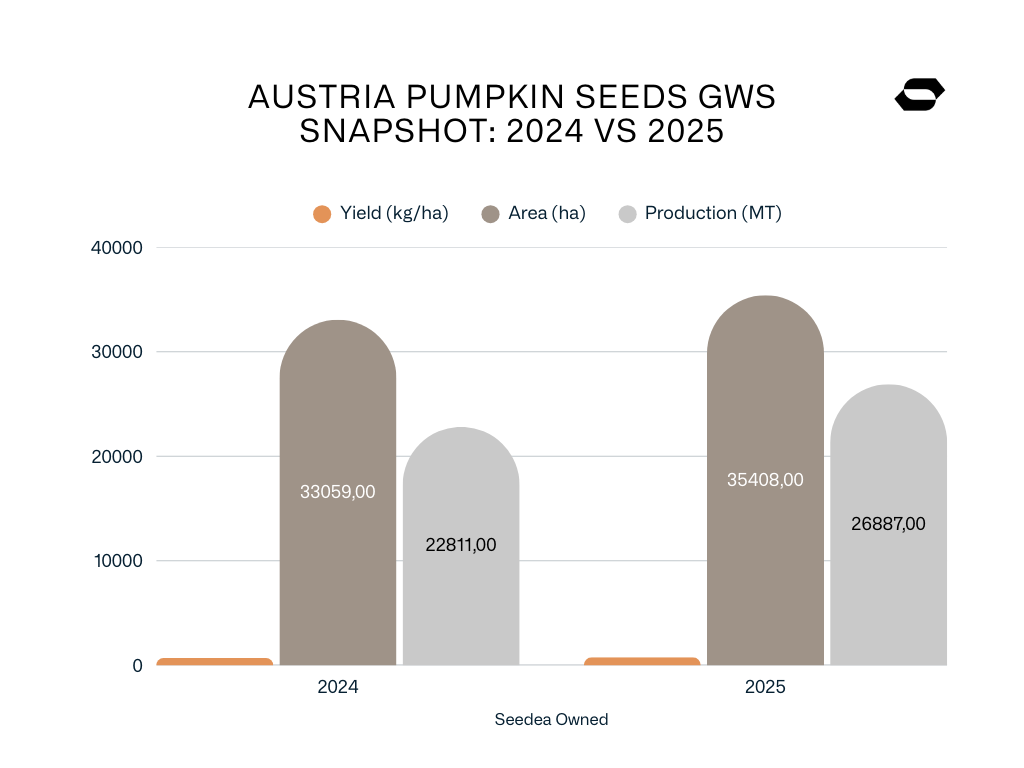

Austria: Stable Harvest, Higher Yield, Strong Benchmark Position

Austria confirmed its role as Europe’s benchmark origin for GWS.

In 2025, total pumpkin seed area reached 35,408 ha, compared to 33,059 ha in 2024. Harvested volume increased to 26,887 MT, versus 22,811 MT in 2024. Average yield improved from 690 kg/ha in 2024 to 760 kg/ha in 2025.

This is a positive signal. However, yield performance varied regionally. Some areas reported clearly below-average productivity, while others performed better. The final average still exceeded last year by 70 kg/ha.

Lower Austria remains the largest pumpkin-producing region, with 17,216 MT harvested in 2025. Styria, the origin of Styrian GWS, produced slightly above 6,500 MT.

Austria maintains one of the highest organic shares in plant production within the EU. Organic pumpkin seed production follows this structural strength. The primary market remains domestic consumption and DACH countries.

Austria sets the quality benchmark for European GWS. When Austrian supply is stable, the entire EU pricing structure stabilises. When supply tightens, price spreads widen quickly.

Poland: Growing GWS Player, Strong Domestic Raw Material Demand

Poland remains the EU leader in total pumpkin production, with nearly 400000 MT annually. However, most of this volume is not dedicated to seed production.

For GWS, the relevant segment is pumpkin grown for seeds purposes and not the flesh. According to ARiMR estimates, pumpkin cultivation area in Poland exceeded 10,000 ha in 2025. Producers estimate GWS harvest at 13,000-15,000 MT in 2025, while 2024 production was approximately 10% lower.

Poland is increasingly perceived as a structural alternative to Chinese GWS supply. Buyers value shorter logistics chains and reduced compliance risk.

However, 2025/2026 shows strong domestic and regional competition for raw material. Austrian and German traders actively source in Poland. This increases raw seed prices and tightens availability.

In the last 2–3 weeks, we observed intensified buying activity. Farmers currently offer prices even €0.20–0.40/kg higher than one month ago. Market momentum clearly supports growers.

Poland has growth potential. However, to challenge Austria structurally, the country needs further development of dedicated seed production and breeding infrastructure.

Organic Pumpkin Seeds: EU-Origin Focus Continues

The organic pumpkin seeds market behaves differently this season. Demand pressure is slightly lower than last year. One reason may be improved harvest performance in Austria and better raw material availability in the EU.

At the same time, Chinese organic GWS remains problematic. In recent years, many shipments faced compliance challenges when entering the EU market. Chinese growers show limited interest in expanding GWS production in general and organic even more. As a result, EU buyers proactively shifted toward EU origins. Austria and Poland became the preferred supply bases.

Organic product is still available. However, as the season progresses, availability will gradually decrease. Prices remain relatively stable at the moment, compared to the last season prices at the same stage of the season.

Pumpkin GWS Market Summary

The conventional GWS market is clearly heated. European buyers are actively reducing exposure to China and shifting structurally toward EU origins. Apart from Austria and Poland, only limited volumes are available in Hungary, Serbia or Croatia, which increases pressure on the European raw material base.

Strong demand is pushing prices higher, especially in Poland, where Austrian and German traders are sourcing aggressively. In recent weeks, raw seed offers increased by €0.20-0.40/kg compared to the previous month. Farmers benefit from the situation, and the market momentum remains upward.

Looking ahead to 2026, planting decisions in China and the EU will be critical. If Poland continues investing in breeding and structured seed production, its role in the European GWS market may expand significantly. In pumpkin market – disciplined procurement and early coverage protect more value than reactive buying.

If you are reviewing your Q2 or Q3 strategy, this is the moment to contact us.

Source:

- https://www.mundus-agri.eu/news/pumpkin-seeds-chinese-year-supports-prices.n36468.html

- https://steiermark.orf.at/stories/3318571/

- https://stmk.lko.at/k%C3%BCrbisanbau-2025-klimawandel-schl%C3%A4gt-voll-durch%2B2400%2B4285149

- https://www.trade.gov.pl/en/news/poland-strengthens-its-position-as-a-leader-in-pumpkin-production-in-the-european-union/